Published on 2021-09-16

As financial technologies evolve and new platforms emerge, invoice finance is subject to rapid digitalisation. Companies are moving trade documents and their exchange online, and this creates new, more efficient methods of factoring. This new breed of financing is called electronic factoring, or e-factoring.

Trade finance requires detailed scrutiny of the documents underlying the transactions as well as the relevant payment information. Supply agreements, delivery notes and invoices are reviewed to identify financing data (nature of financed goods, amounts, currencies) and prevent fraud. Payment data must be tracked to uncover discrepancies in amounts and overdue payments.

Manual checks lead to high administrative costs and delays in outpayments. Consequently, paper/scan-based factoring may be prohibitively expensive and slow to finance certain transactions, especially those that are smaller or cross borders. E-factoring changes that.

Handling documents in digital form enables Robotic Process Automation (RPA), resulting in cost and time savings. Instead of exchanging scanned documents or their physical copies, Electronic Documentary Interchange (EDI) solutions allow companies to work with electronic originals. In addition, bank account integrations optimise making payments and tracking settlements.

Electronic documents are typically machine-readable, which allows financiers to quickly identify the amounts and currencies involved. It’s also possible to meet requirements more easily, recognising goods from the digital agreement or itemised invoices. Financiers can now quickly see if goods in the transaction are SRI-restricted or sanctioned. Similarly, it’s possible to assess whether the goods are eligible for lower-cost financing from ESG-focused funders.

The authenticity of electronic originals can be verified more easily as they stem from the primary channel of data exchange and cannot be manipulated. Such documents often bear the electronic signatures of company representatives, helping determine if approvals have been given by authorised personnel. In other words, digitalisation helps prevent fraud.

Electronic invoicing and APIs lead to significant savings in executing and monitoring payments. Factors can send machine-readable payment orders to their bank or even initiate payments from their own systems. Similarly, APIs allow the tracking of settlements and the automatic flagging of exceptions and late payments. This means financiers can enhance collections by working with fewer errors and faster response times.

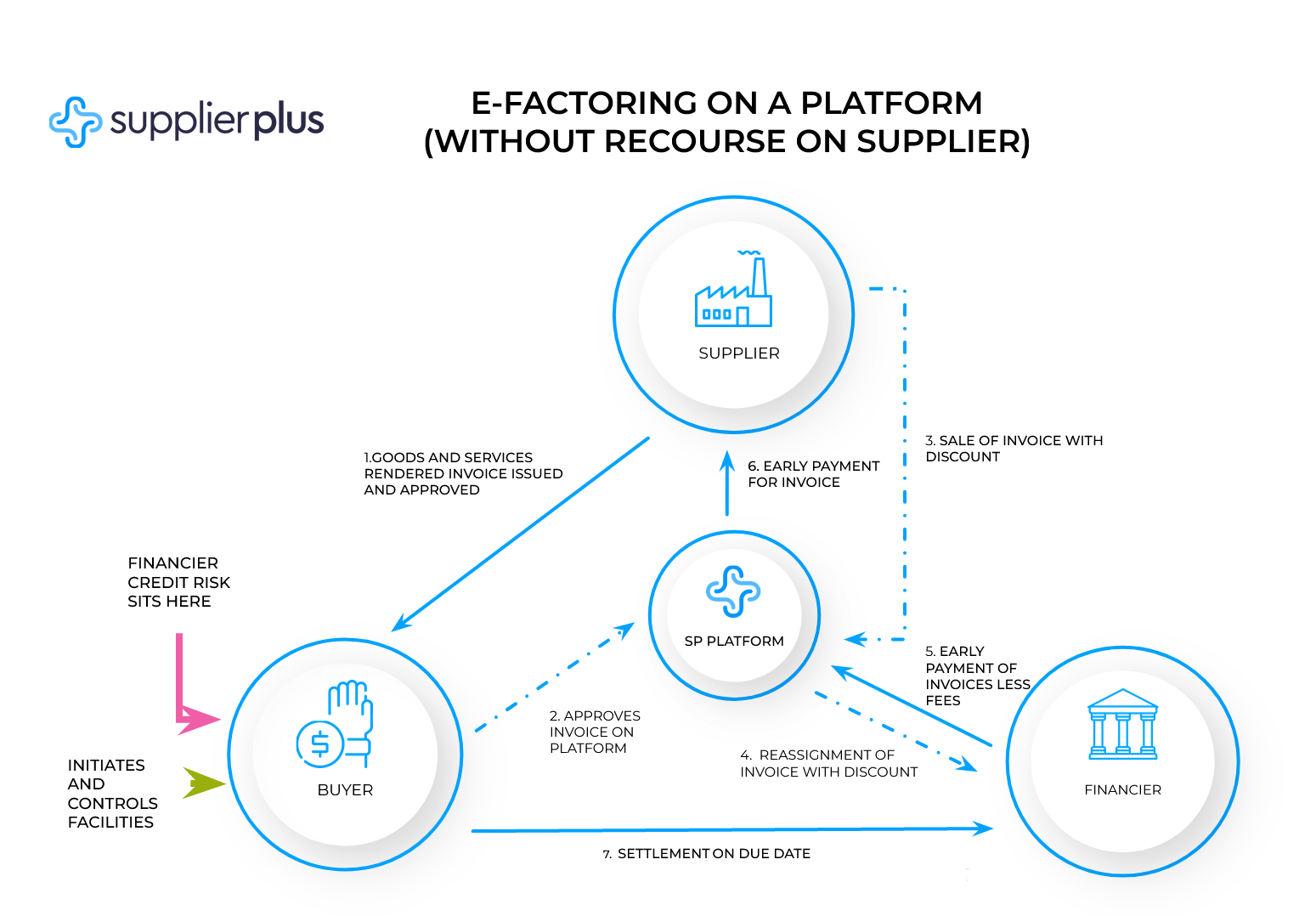

Ultimately, e-factoring can significantly speed up transaction times, reduce labour costs and mitigate risks of fraud, meaning merchants benefit from faster and more affordable access to working capital. A detailed diagram on how electronic factoring works on a platform is presented below (see Diagram 1).